Institutional Insights: BofA G10 FX Ceasefire Flows & Positioning

G10 FX Flows & Positioning

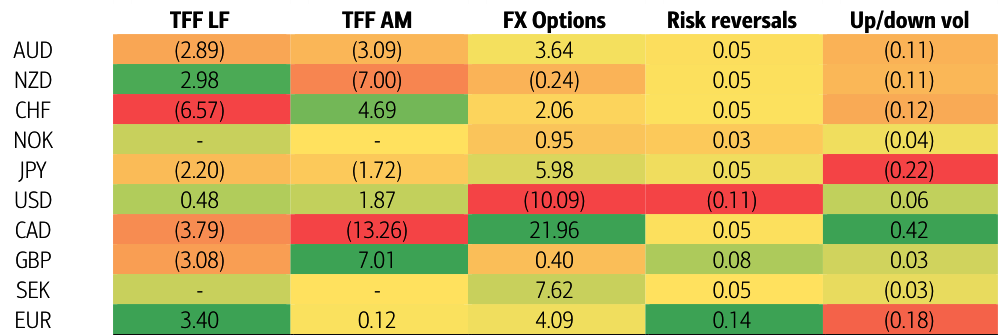

Ceasefire-related flows have supported parts of European FX, particularly EUR, SEK and GBP, but the broader USD picture is more mixed than the spot move alone would suggest. Since the ceasefire announcement, flow dynamics indicate demand for EUR, SEK and GBP versus AUD, NZD and CHF, while post-war USD demand has only partially unwound and started from a backdrop of already net short USD positioning. That matters because the Dollar sell-off has not come from a market that was materially long USD to begin with, limiting the extent of any clean capitulation story. On that basis, the near-term bias still leans constructive USD, especially against less heavily sold currencies such as CAD and GBP.

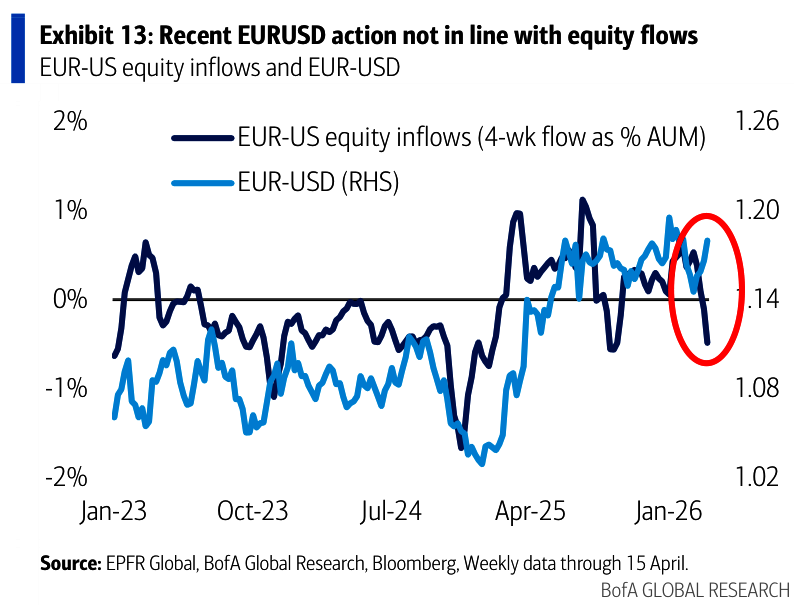

In options, the recent pattern has been more clearly USD-negative, with a near-dated flow showing USD supply versus CAD, SEK, JPY, and especially EM FX. Net USD positioning has turned slightly short, though still remains less short than pre-war levels, while AUD longs and GBP shorts continue to stand out as the clearest residual positioning imbalances. In futures, the signal is more nuanced: there has been net EUR demand, particularly from leveraged funds, but not clearly at the expense of USD in aggregate. USD positioning looks broadly neutral among leveraged funds but remains short among asset managers. Meanwhile, up/down vol and risk reversals suggest USD longs have been reduced across G10 since the ceasefire, with EUR benefiting the most from the change in skew. At the same time, broader volatility-based positioning measures imply EUR positioning may still not be especially long in outright terms, which helps explain why EURUSD has remained supported. One important caveat is that equity flow signals have recently turned USD- and CAD-supportive and EUR-negative, which looks somewhat inconsistent with spot price action and suggests current EURUSD resilience may be more fragile than it appears.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!